Exercise: Multivariate Linear Regression

In this exercise, you will investigate multivariate linear regression

using gradient descent and the normal equations. You will also examine

the relationship between the cost function ![]() ,

the convergence of gradient descent, and the learning rate

,

the convergence of gradient descent, and the learning rate ![]() .

.

Data

Download

ex3Data.zip, and extract the files from the zip file.

This is a training set of housing prices in Portland, Oregon,

where the outputs ![]() are the prices and the inputs

are the prices and the inputs ![]() are

the living area and the number of bedrooms. There are

are

the living area and the number of bedrooms. There are ![]() training examples.

training examples.

Preprocessing your data

Load the data for the training examples into your program and add

the ![]() intercept term into your x matrix. Recall that the command

in Matlab/Octave for adding a column of ones is

intercept term into your x matrix. Recall that the command

in Matlab/Octave for adding a column of ones is

x = [ones(m, 1), x];

Take a look at

the values of the inputs ![]() and note that the living areas

are about 1000 times the number of bedrooms. This difference means that

preprocessing the inputs will significantly increase gradient descent's

efficiency.

and note that the living areas

are about 1000 times the number of bedrooms. This difference means that

preprocessing the inputs will significantly increase gradient descent's

efficiency.

In your program, scale both types of inputs by their standard deviations and set their means to zero. In Matlab/Octave, this can be executed with

sigma = std(x); mu = mean(x); x(:,2) = (x(:,2) - mu(2))./ sigma(2); x(:,3) = (x(:,3) - mu(3))./ sigma(3);

Gradient descent

Previously, you implemented gradient descent on a univariate regression problem. The only difference now is that there is one more feature in the matrix x.

The hypothesis function is still

|

and the batch gradient descent update rule is

|

Once again, initialize your parameters to

![]() .

.

Selecting a learning rate using ![]()

Now it's time to select a learning rate ![]() The goal of this part is to pick a good

learning rate in the range of

The goal of this part is to pick a good

learning rate in the range of

|

The cost function can also be written in the following vectorized form,

![\begin{displaymath}

\begin{array}{cc}

\par

\vec{y} = \left[

\begin{array}{c}

y...

...m)})^T\mbox{-}

\end{array}\right] \nonumber

\par

\end{array}\end{displaymath}](img14.png) |

The vectorized version is useful and efficient when you're working with numerical computing tools like Matlab/Octave. If you are familiar with matrices, you can prove to yourself that the two forms are equivalent.

While in the previous exercise you calculated ![]() over a grid of

over a grid of ![]() and

and ![]() values, you will now calculate

values, you will now calculate ![]() using the

using the ![]() of the current stage of gradient descent. After stepping through many stages,

you will see how

of the current stage of gradient descent. After stepping through many stages,

you will see how ![]() changes as the iterations advance.

changes as the iterations advance.

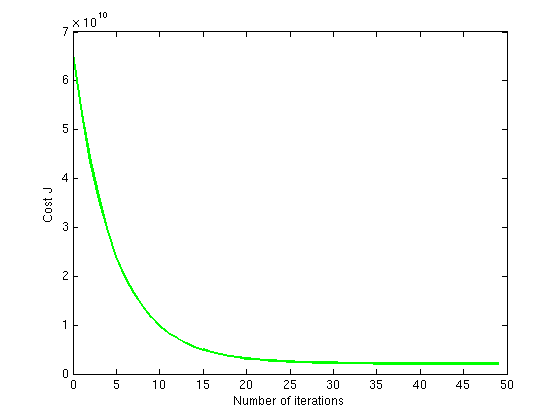

Now, run gradient descent for about 50 iterations at your initial learning rate. In each

iteration, calculate ![]() and store the result in a vector J. After the last iteration,

plot the J values against the number of the iteration. In Matlab/Octave, the steps would

look something like this:

and store the result in a vector J. After the last iteration,

plot the J values against the number of the iteration. In Matlab/Octave, the steps would

look something like this:

theta = zeros(size(x(1,:)))'; % initialize fitting parameters

alpha = %% Your initial learning rate %%

J = zeros(50, 1);

for num_iterations = 1:50

J(num_iterations) = %% Calculate your cost function here %%

theta = %% Result of gradient descent update %%

end

% now plot J

% technically, the first J starts at the zero-eth iteration

% but Matlab/Octave doesn't have a zero index

figure;

plot(0:49, J(1:50), '-')

xlabel('Number of iterations')

ylabel('Cost J')

If you picked a learning rate within a good range, your plot should appear like the figure below.

If your graph looks very different, especially if your value

of ![]() increases or even blows up,

adjust your learning rate and try again.

We recommend testing alphas at a rate of of 3 times the

next smallest value (i.e. 0.01, 0.03, 0.1, 0.3 and so on).

You may also want to adjust

the number of iterations you are running if that will help you see

the overall trend in the curve.

increases or even blows up,

adjust your learning rate and try again.

We recommend testing alphas at a rate of of 3 times the

next smallest value (i.e. 0.01, 0.03, 0.1, 0.3 and so on).

You may also want to adjust

the number of iterations you are running if that will help you see

the overall trend in the curve.

To compare how different learning learning rates affect convergence, it's helpful to plot J for several learning rates on the same graph. In Matlab/Octave, this can be done by performing gradient descent multiple times with a 'hold on' command between plots. Concretely, if you've tried three different values of alpha (you should probably try more values than this) and stored the costs in J1, J2 and J3, you can use the following commands to plot them on the same figure:

plot(0:49, J1(1:50), 'b-'); hold on; plot(0:49, J2(1:50), 'r-'); plot(0:49, J3(1:50), 'k-');

The final arguments `b-', `r-', and 'k-' specify different plot styles for the plots. Type

help plot

at the Matlab/Octave command line for more information on plot styles.

Observe the changes in the cost function happens as the learning rate changes. What happens when the learning rate is too small? Too large?

Using the best learning rate that you found, run gradient descent until convergence to find

1. The final values of ![]()

2. The predicted price of a house with 1650 square feet and 3 bedrooms. Don't forget to scale your features when you make this prediction!

Normal Equations

In the Normal Equations video, you learned that the closed-form

solution to a least squares fit is

1. In your program, use the formula above to calculate ![]() . Remember that

while you don't need to scale your features, you still need to add

an intercept term.

. Remember that

while you don't need to scale your features, you still need to add

an intercept term.

2. Once you have found ![]() from this method, use it to make a price prediction for a 1650-square-foot house with 3 bedrooms.

Did you get the same price that you found through gradient descent?

from this method, use it to make a price prediction for a 1650-square-foot house with 3 bedrooms.

Did you get the same price that you found through gradient descent?